Executive Summary: Helping youngsters start a Roth IRA is a powerful way to set them up for long-term financial success. Even small contributions, left to compound over decades, can grow significantly. With no required withdrawals and tax-free growth, a Roth IRA is an invaluable gift that keeps on giving.

While many of us talk about taking an early retirement, we rarely contemplate the idea of making one for someone else. In particular, how about making one (or at least starting one) for a young family member or friend—yes, even someone as young as a teenager?

It’s tax season, and the window to contribute to retirement accounts based on last year’s (2024) earnings is closing fast. So, as I do every year, let me tell you that even teenagers can have a retirement account. They may not be ready to put aside money for their much older self—and I’m not here to fault them for that—but that doesn’t mean you can’t do it for them.

I write about this topic every year because I’ve seen the benefits firsthand. My parents funded a Roth IRA on my behalf during my teenage years—thank you! My mentor, who also wrote about the strategy, funded IRAs for his children when they were teenagers.

Helping a young person prepare for retirement may not get you many high-fives or fist-bumps today. But trust me, the beneficiary of your forward-thinking will thank you for years to come as they move into and through adulthood.

How a Teen IRA Works

It’s pretty simple. Once someone starts earning income, they can contribute to a retirement account. Even if that earner is a teenager working part-time or picking up a summer job, they can start building a retirement nest egg.

However, you must report the income to the IRS for it to count. If your neighbor is paying your teenager cash for babysitting now and again and you aren’t reporting those earnings, you can’t contribute to a Roth IRA on behalf of your child.

[Clarification: Depending on how much the child earned, its possible to contribute to a Roth IRA without filing taxes. However, the income must be real, traceable and documented (think, a W-2).]

A young person (anyone under 50, according to the IRS) can contribute earnings of as much as $7,000 to a Roth IRA. Make just $2,500 working this summer, and they can put $2,500 into a Roth IRA. Earn $10,000 working part-time, year-round, and their contribution is capped at $7,000.

Do I really expect a teenager to save for retirement? No, but that doesn’t mean we “elders” can’t help them!

Let’s assume you can afford to match your teen’s summer earnings. Do it. Let them have their hard-earned money, but open a Roth IRA in your child's or grandchild’s name and add the money yourself. (Though it doesn’t have to be a family member. You can do this for any teen you want to help out.)

Maybe you can’t afford to add the whole amount. Consider making a deal with your teen to match a portion or a multiple of any earnings they add to the Roth IRA. If the teen contributes $250, maybe you’ll contribute $500 or $1,000. I’ll show you how even small contributions add up over decades.

Heck, even if you can afford the whole amount, having your teen contribute something to the pot may be a good idea—it’s a learning opportunity and gives them buy-in.

Roth over Traditional

I was intentional when I wrote “Roth IRA” in the paragraphs above because they are a better choice for younger people than traditional IRAs.

Traditional and Roth IRAs are powerful accounts where you can compound your earnings tax-free. But, of course, you have to have a long-term mindset. The money contributed is generally locked up until the IRA’s beneficiary is 59 ½ years old—unless they feel like paying a 10% fee on withdrawals.

There are some exceptions to that penalty—for instance, if the distributions are used for a first-time home purchase (something today’s kid might appreciate down the road) or to help with a disability—but really, you shouldn’t expect this money to be touched for years and years. Once clear of the age of 59½, that 10% penalty disappears.

However, Roth IRAs have a clear advantage over traditional IRAs—though, again, your teen won’t understand why until they are well down the retirement road. The advantage is withdrawals.

A traditional IRA forces you to take distributions in retirement (for today's teens, that means the age of 75), paying income taxes at your future (and possibly higher) tax rate. With a Roth IRA, once you hit retirement, there is no distribution requirement—if you don’t feel like taking money out or don’t need it, you can leave it to continue growing tax-deferred. And if you do make withdrawals, they are entirely tax-free.

Also, it’s worth noting that the owner of a Roth IRA can withdraw contributions at any time, tax- and penalty-free, after five years. Since taxes have already been paid on the contributions, they won’t be taxed again. The earnings would be taxed and subject to a penalty if an early (pre-59½) distribution is taken.

To be clear, I’d strongly discourage anyone from doing this—the ability to compound tax-free for years is so powerful. But the option is there.

The bottom line is that putting money in a Roth IRA, where a teen can leave it to compound tax-free indefinitely and avoid paying taxes on withdrawals in retirement, is a gift they will (one day) appreciate greatly.

Spending Decades in the Market

The power of compounding makes funding a teen’s Roth IRA an intelligent investment.

I’ve written several articles—like Compounding Takes Time and Put Time on Your Side—demonstrating the benefits of saving and investing early. It takes patience and discipline, but compounding works over time. (Feel free to share this and either of those articles with any young person you are encouraging to start investing.)

But let me show you the value of helping a teen get an early start on funding their retirement—even if you can only help a little for a limited time.

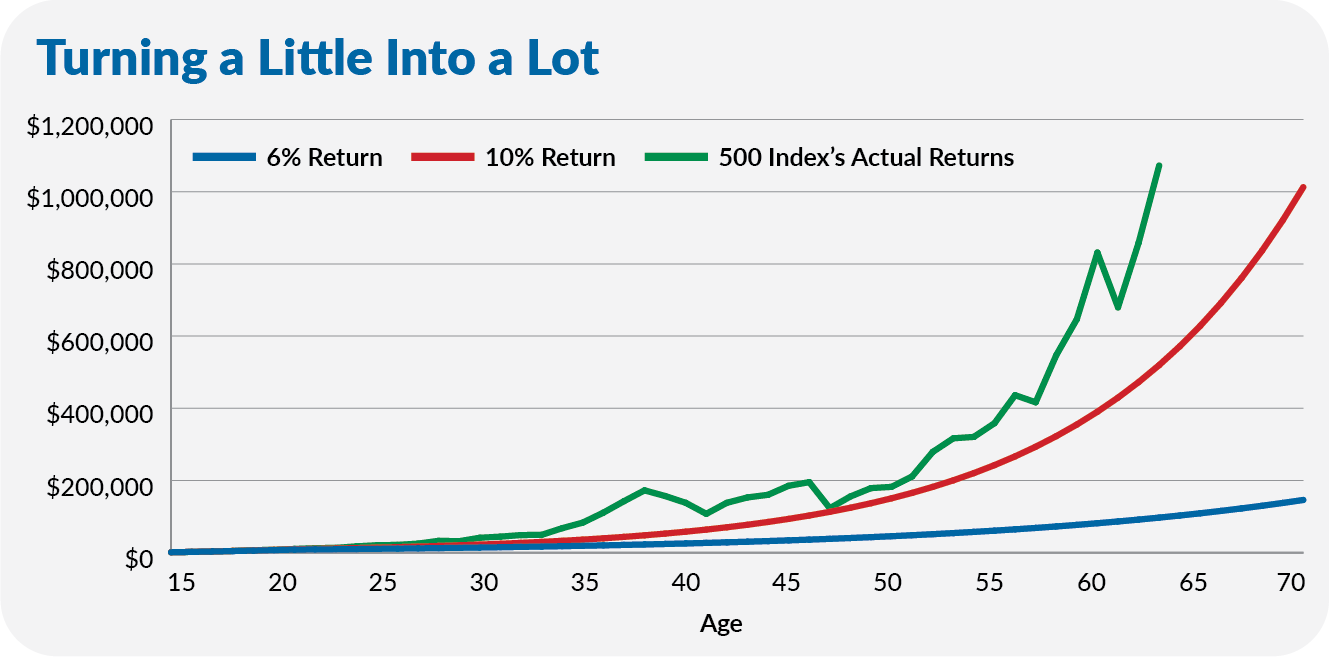

Let’s say your teen starts their first summer job at age 15 and continues to hold it through college (age 22). You can contribute $1,000 to their Roth IRA each year for those seven years, for a total of $7,000.

Would it be worth it if another penny was never added to the account? Absolutely.

Consider the chart below, where I’ve plotted the growth of our teen’s portfolio over time, assuming different rates of return.

Even if your teen’s money goes on to only compound at a 6% annual rate, they’ll turn that $7,000 into over $80,000 by the time they turn 60 (and can start withdrawing it penalty-free). If they leave the money untouched and it continues to grow 6% per year for another decade, they’ll have around $145,000 in the account on their 70th birthday. Not too shabby.

The results are even more compelling if your teen earns better returns. Stocks have historically compounded around 10% per year. Compound at 10% a year, that $7,000 contribution becomes nearly $400,000 on your no-longer-a-teen’s 60th birthday. Give it another ten years, and we’re looking at a portfolio worth a million dollars.

Of course, stocks don’t go up in a straight line, so in the chart above, I’ve included the actual results of an investment made in 500 Index (VFINX/VFIAX) starting with the index fund’s first full calendar year (1977). Again, only $1,000 was contributed in each of the first seven years.

We don’t have enough history to get to age 70 in this example, but as you can see, the actual returns of 500 Index are tracking above the smooth 10% annual return scenario. That’s no surprise, as 500 Index compounded at an 11.4% annual rate between 1977 and 2024.

Even if you can’t contribute the full annual amount ($7,000) and don’t know if your young adult will follow your lead, doing what you can today is worth it. As long as the money is left in the account and allowed to grow tax-free, compounding can turn a little into quite a lot if given decades to work.

I’ve taken this example further in the appendix, but let’s discuss what to do once the money is in the account.

What to Buy

After you’ve funded your teen’s Roth IRA, you must decide where to invest. Here is the guide for investors starting their investment journey I recently shared.

Let me give you the Cliff’s Notes version:

When initially funding your teen’s Roth IRA, you may have to contend with the fact that most Vanguard mutual funds require a $3,000 investment to get in the door.

To bypass this investment hurdle, you can buy an ETF—the minimum amount you need is the price of one share. Since we’re talking about a young investor with years and years ahead of them, go with a stock ETF.

You can’t go wrong picking S&P 500 ETF (VOO), Total Stock Market ETF (VTI), Total International Stock ETF (VXUS) or Total World Stock ETF (VT)—or mix and match as you see fit.

Amongst Vanguard’s mutual funds, your low-minimum ($1,000) options are STAR (VGSTX) or the Target Retirement funds. They are better than leaving the money in cash, but a significant drawback of these options is that they invest a portion of the assets in bonds. Your teen’s retirement is decades away, so they shouldn’t hold bonds in this account.

Of course, following one of the IVA Portfolios would be another solution. However, you need around $5,000 to follow the Aggressive ETF Portfolio and about $15,000 to track the Aggressive Portfolio (if you use the ETF versions of the small-stock and real estate funds).

Also, if your teen is interested in the markets, this is a perfect place and time to let them call a few of the shots. Do they have a favorite brand? Maybe they want to buy some stock in the company.

As the account grows, you (or your teen) may want to consider a portfolio that isn’t constrained to “low-minimum” funds. But you can cross that bridge when you come to it. Remember, in a Roth IRA, you don’t have to worry about the impact of taxes when repositioning (or trading) your portfolio.

All Aboard

Time is on a kid’s side, and by helping one start to build a Roth IRA with earnings from summer and part-time jobs, you may be able to make a meaningful impression on them. Not only are you booking them an early seat aboard the retirement train, but you are also helping them develop lifelong habits (of saving and investing) that will stand them in good stead as they pass into and through their working years.

So, tote up what Mr. or Ms. Gen Z earned in 2024 and fund that IRA account before the April deadline. And if they didn’t work last year but are picking up their first summer job this year, now is a great time to have a conversation about what they are going to do with their earnings.

Helping to put your teenage—or just newly employed—child or grandchild on the road to a more comfortable retirement may be one of the best gifts you can give, and it will keep on giving year after year.

Appendix.

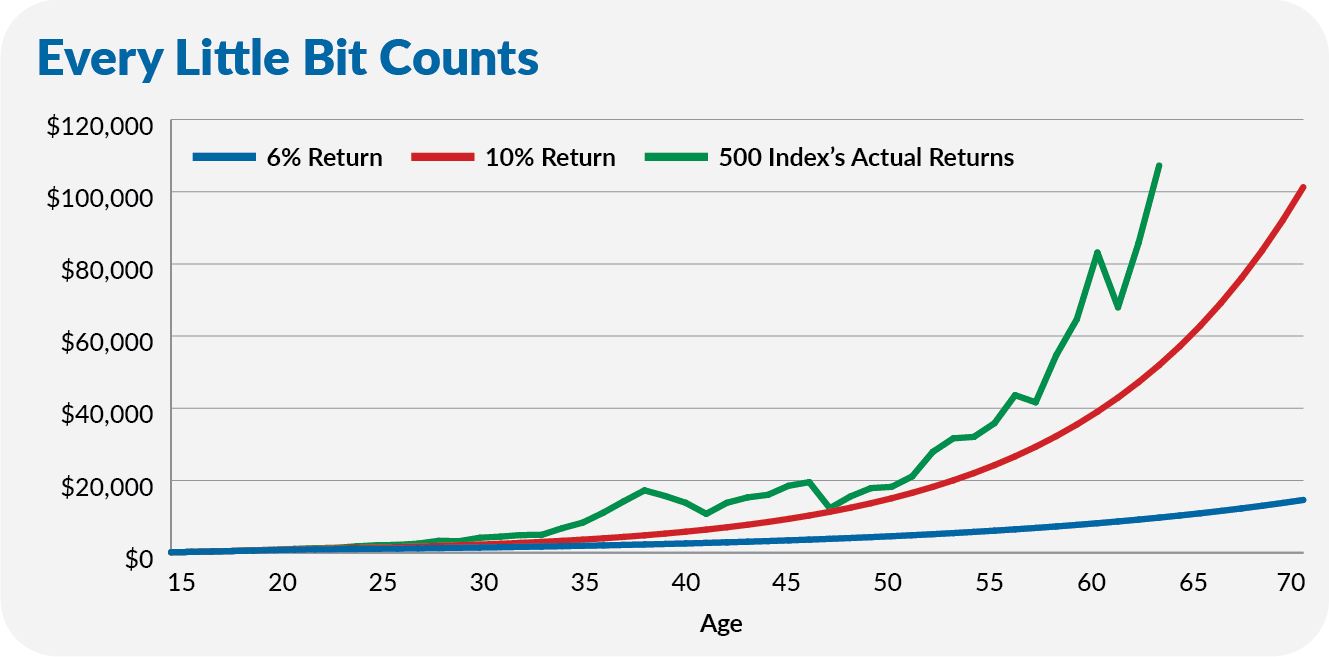

Let’s take my example of giving a little help for a limited amount of time even further. Instead of contributing $1,000 each year to your teen’s Roth IRA, what if you only contribute $100? Again, you’ll only contribute that money for seven years while they are in high school and college.

The chart below shows what those $700 in contributions earning 6%, 10% and the actual returns of 500 Index look like over the course of a lifetime.

At a 10% annual rate, those $700 turn into nearly $40,000 by age 60. A decade later, we’re talking about $100,000. Are there any 70-year-olds who would turn down an extra 100,000 tax-free dollars?

The numbers are more impressive for 500 Index’s actual returns but are less so at the lower 6% return. Still, the point stands. Time in the market pays off—and the more time, the better. So, start investing early, even if only a few dollars.