FUNDS FOCUS — TAX-FREE BOND FUNDS | Evaluating Vanguard’s bond options for tax-sensitive investors.

Executive Summary: Vanguard’s municipal bond funds offer tax-sensitive investors a way to keep more of their earnings. This guide explores top picks, tax-equivalent yields and smart swaps for taxable bonds. With solid returns and low risk, muni bonds can be a core holding in your taxable brokerage account.

Taxes are a cost. Let’s be clear about that. Taxes reduce the income and capital gains you and I hold onto. And as with all costs, keeping them low is good practice. Municipal bonds are one way to do that.

As Vanguard investors, you and I have some great tax-free bond funds to choose from. Vanguard has been adding more options of late, which can make choosing the right fund more difficult. So, here’s my take on all of Vanguard’s tax-exempt bond funds.

If you need a refresher on muni bonds, check out Muni Bonds 101.

Tax-Free Substitutes for Current IVA Portfolio Holdings

Municipal Money Market (VMSXX): A stable price with a decent tax-free income.

Intermediate-Term Tax-Exempt (VWITX): Best core holding that balances risk and return well.

Also Great …

Ultra-Short-Term Tax-Exempt (VWSTX): Best cash alternative for money you aren’t spending immediately.

An Up and Comer ...

Core Tax-Exempt Bond ETF (VCRM): An actively managed ETF that owns a broad array of municipal bonds.

My Top Picks

If you’re a tax-sensitive investor tracking one of my balanced Portfolios (which own some bond funds), you can opt to replace Federal Money Market (VMFXX) and Intermediate-Term Treasury (VFITX) with Municipal Money Market (VMSXX) and Intermediate-Term Tax-Exempt (VWITX). I’ll discuss some alternatives, but those replacements apply to most investors.

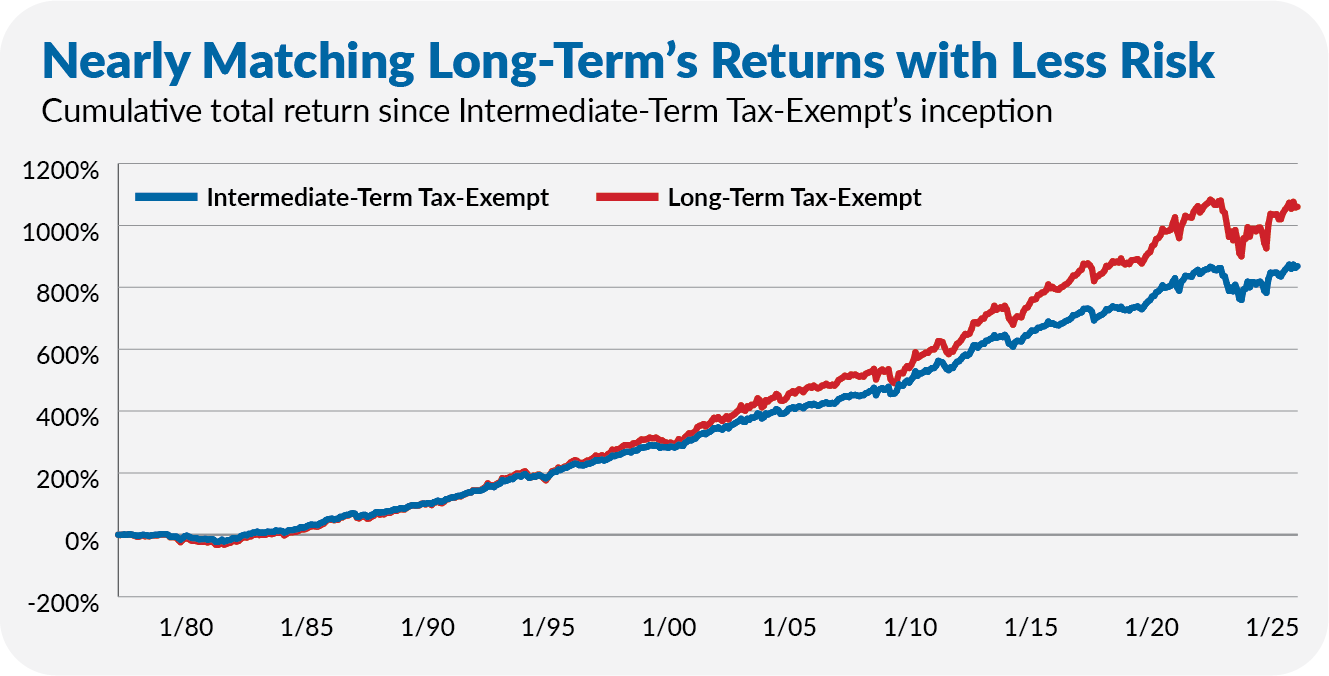

All of Vanguard’s tax-exempt bond funds are strong options. But if I had to pick just one fund, it would be Intermediate-Term Tax-Exempt (VWITX).

Intermediate-term bonds have long balanced the risks and rewards of investing in the fixed-income markets well. Over its 47-year history, Intermediate-Term Tax-Exempt has delivered about 80% of the return of Long-Term Tax-Exempt (VWLTX) while taking on a third less risk.

That’s a balancing act worth investing in.

Source: Vanguard and The IVA

Of course, Intermediate-Term Tax-Exempt is not the only middle-maturity muni fund Vanguard offers. Intermediate-Term Tax-Exempt Bond ETF (VTEI) is my first choice as a substitute for Intermediate-Term Tax-Exempt for index-adherents.

I also don’t have a problem if index investors use Tax-Exempt Bond ETF (VTEB or VTEAX) instead of the active mutual fund. But, between the two, the newer intermediate-term bond ETF is a better match for Intermediate-Term Tax-Exempt.

And if you’re looking for another alternative, the recently launched Core Tax-Exempt Bond ETF (VCRM) is my pick as Vanguard’s top up-and-coming municipal bond fund. You get Vanguard’s active management expertise in a low-cost ETF wrapper. There’s a lot to like, and I expect it will compete well with Intermediate-Term Tax-Exempt over time.

So, that’s how a tax-sensitive investor can think about replacing Intermediate-Term Treasury (VFITX) in the IVA Portfolios.

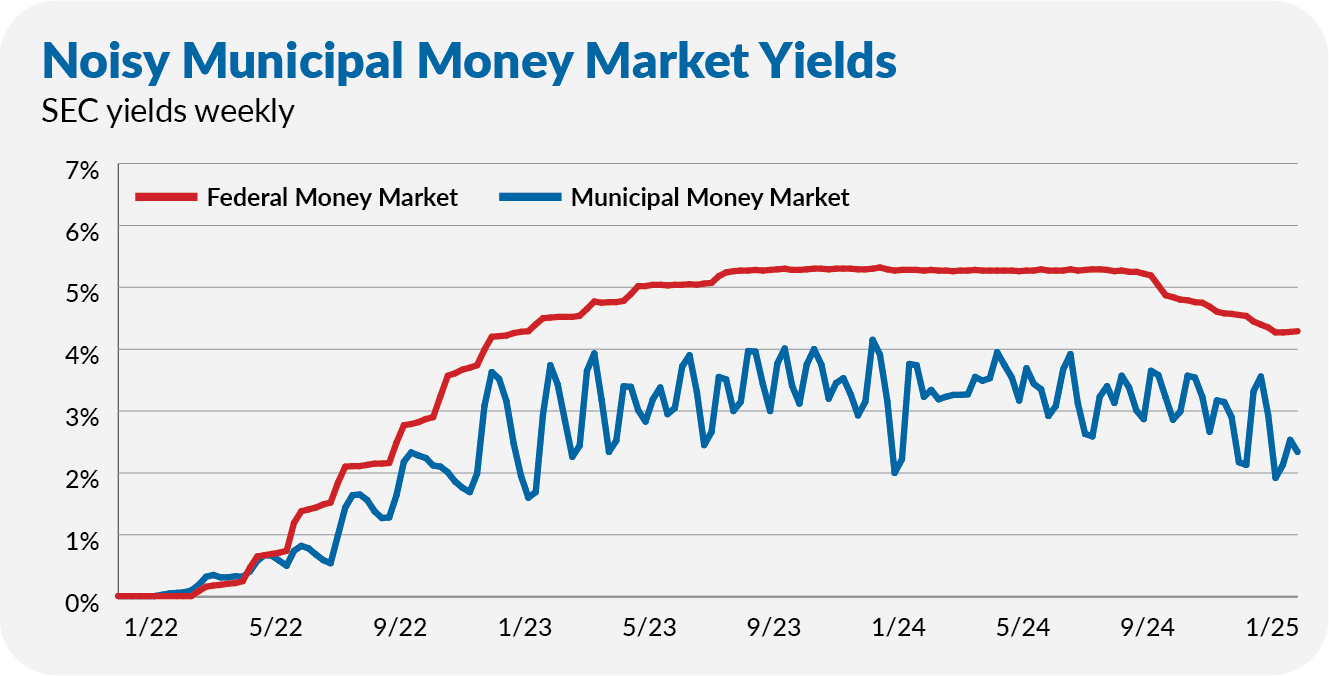

Turning to the other IVA bond holding, Federal Money Market (VMFXX). Just keep it simple and use Municipal Money Market (VMSXX), which pays a decent amount of income while providing stability to the Portfolios. If you’re an investor in California or New York, consider using the state-specific money market funds. (For the record, I own New York Municipal Money Market (VYFXX).)

If you go with one of the municipal money market funds, I caution against chasing the noise. As the chart below shows, Municipal Money Market’s yield on a weekly basis is much noisier (more volatile) than Federal Money Market’s. (The reason why gets into the nitty gritty of the municipal bond market. The short answer is supply and demand—there are fewer tax-exempt bonds available compared to Treasurys, investors jump in and out, etc.)

Source: Vanguard and The IVA

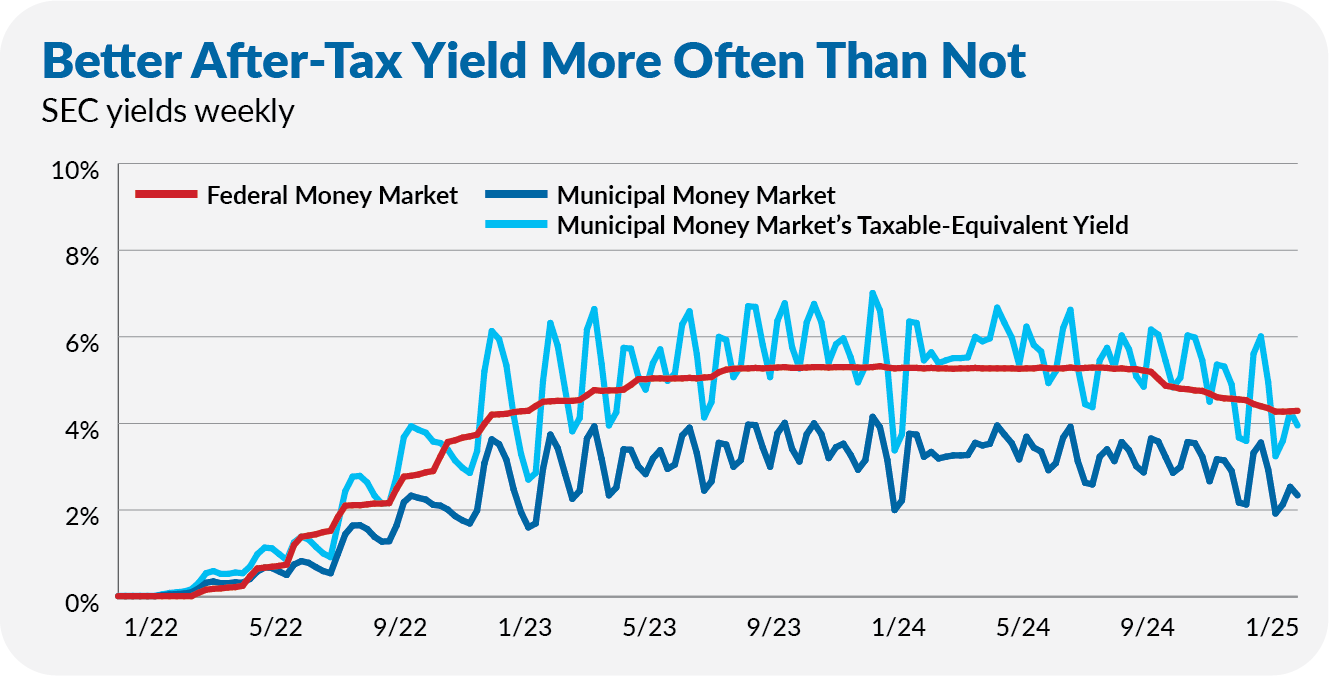

Of course, what matters to tax-sensitive investors is not the absolute yield but the after-tax yield. In the following chart, I added Municipal Money Market’s taxable-equivalent yield. (I used a tax rate of 40.8%. That’s for someone in the 37% tax bracket plus a 3.8% health care surtax.)

For most of the past three years, the tax-sensitive investor has come out ahead after taxes with the municipal money market fund—the dotted line is above Federal Money Market’s yield.

Source: Vanguard and The IVA

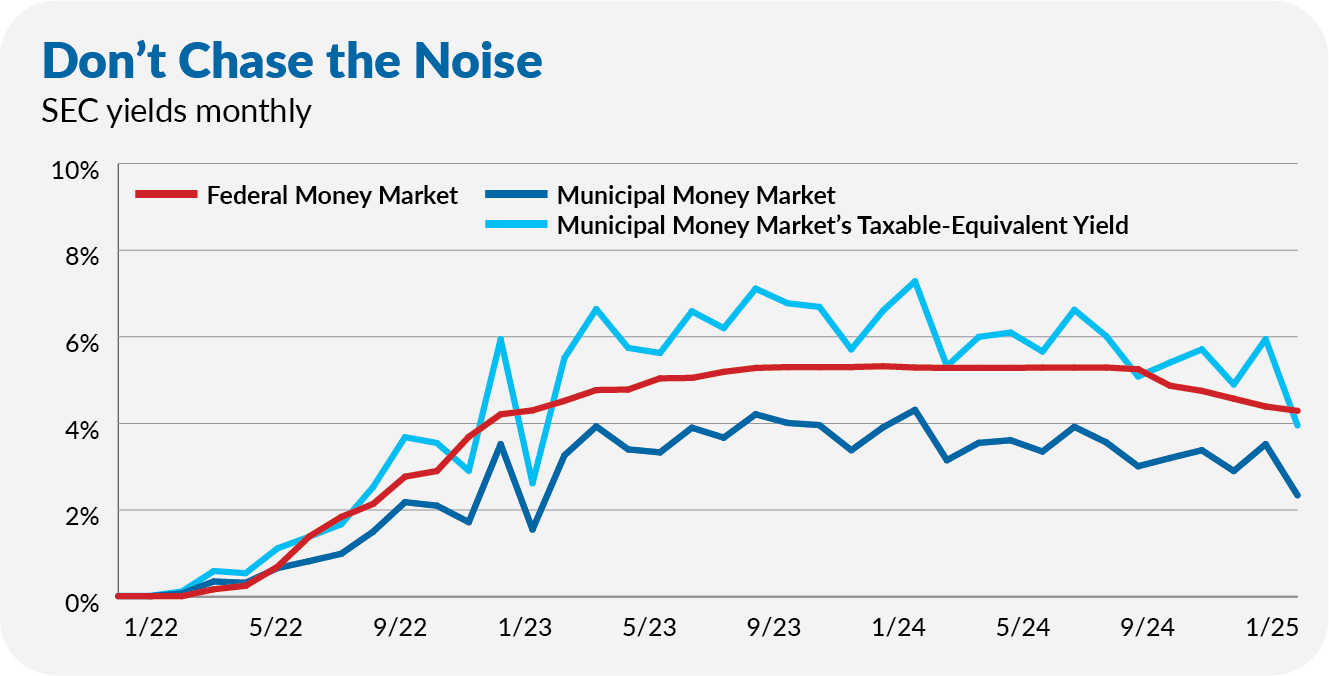

Yes, there were moments to swap between the two—when Federal Money Market offered a better yield despite the higher tax burden. However, those moments were fleeting. Below is the same chart but showing monthly yields. The municipal fund’s yield still moves around more, but it was consistently the pick for tax-sensitive investors.

Source: Vanguard and The IVA

So, if you have a very large cash pile and an abundance of free time, maybe you’ll spend that time chasing money market yields. But, otherwise, I wouldn’t play the hokey-pokey with the funds. It’s a lot of work for little payoff.

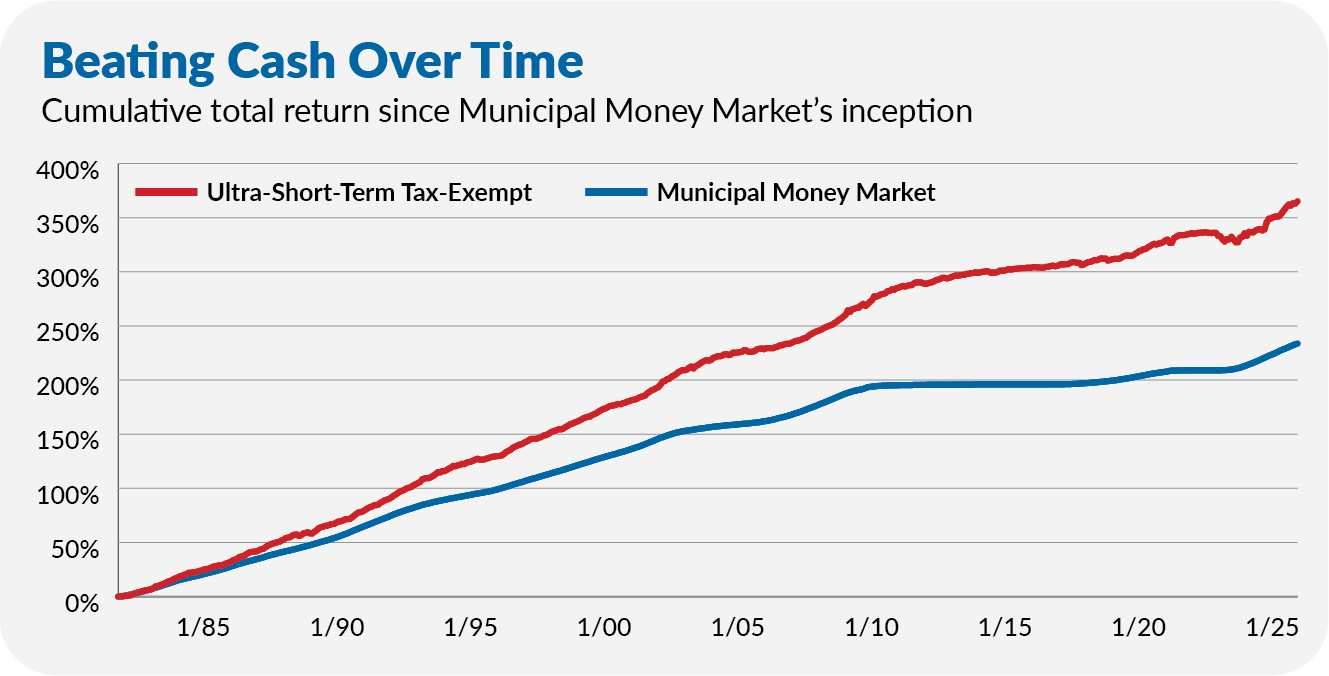

An alternative to holding a money market is (the still great) Ultra-Short-Term Tax-Exempt (VWSTX). The ultra-short fund has a long history of delivering better-than-cash returns to investors willing to take on some risk.

Source: Vanguard and The IVA

I’ve owned Ultra-Short-Term Tax-Exempt before and sold it when the Federal Reserve hiked interest rates and the yield curve inverted. But I could buy it again as the market normalizes. Right now, though, as I explained the other week (here), I prefer to play it safe in the bond market. That means holding some cash in lieu of higher-yielding bonds, no matter how short their maturities.

Are Munis for You?

Before we dig further into the funds, let me provide a framework for helping you decide if municipal bond funds are right for you.

Depending on whom you lend money to (who’s issuing the bond), the interest you receive will either be fully taxable or exempt from certain taxes—sometimes federal-tax-free and sometimes state-tax-free and sometimes both.

When you lend to the U.S. government (think Treasury bonds), your interest is subject to federal income taxes but not state or city income taxes. Corporate bond interest is typically taxed at all levels—federal, state and local.

When you lend to a state or local entity (municipality), the interest income is exempt from federal taxes. And if you live in the same state as the borrower, the income is not taxed by the state. (There are exceptions, but let’s keep it simple.)

These tax-free bonds are also called tax-exempt or municipal (“muni”) bonds.

Since we are talking taxes, this discussion assumes you are investing in your brokerage account. When it comes to tax-deferred accounts (like a 401(k) or an IRA), well, taxes aren’t an issue.

Rule of thumb: If you are in one of the top three tax brackets, consider owning a municipal bond fund in your brokerage account.

If you can earn tax-free income, why would you ever buy a bond that pays you taxable income?

Well, the market isn’t dumb (most of the time), and typically, a municipal bond will pay less income than a corporate bond of similar maturity and default risk. If they had the same yield, an investor would not buy the corporate (taxable) bond. So, typically, a municipal bond yields less than a taxable bond because the income is free from federal (and potentially state) taxes.

To put some numbers on it, you should expect the tax-free fund’s yield to be about 30% to 40% lower than the taxable fund’s yield—most of the time.

Consider the yields of Intermediate-Term Treasury (VFITX), Intermediate-Term Investment-Grade (VFICX) and Intermediate-Term Tax-Exempt (VWITX) on February 12. The municipal fund had a yield of 3.39%. That’s well below the yields of the Treasury fund (4.25%) and the corporate-heavy fund (5.15%)—which is what we’d expect.

So, how do you decide whether to buy a tax-free bond (or fund)? It’s in the math.

Clearly, if you are deciding between buying a taxable bond and a municipal bond, you can’t just look at their stated yields. You need to consider taxes.

A common way to compare taxable and tax-free fund yields on even ground is to calculate a “taxable equivalent yield” for the municipal fund. You would need to earn this yield on a taxable fund to give you the same after-tax yield of the tax-free fund. The formula to make this calculation is:

You don’t have to go through all of the math yourself each time you are deciding between muni and taxable bond funds—I’ve done it for you. Each month, you’ll find tax-equivalent yields in the Performance Review tables, updated with the most recent yield data.

Using data from the end of January, I’ve compiled the table below to help you compare Vanguard’s tax-exempt funds against their taxable siblings.

Competitive Yields on Tax-Exempt Funds

Taxable-Equivalent Yields

Yield

22%

24%

35.8%*

38.8%*

40.8*

Yield

Municipal Money Market

2.34%

3.00%

3.08%

3.64%

3.82%

3.95%

Federal Money Market

4.29%

Ultra-Short-Term Tax-Exempt

2.96%

3.79%

3.89%

4.61%

4.84%

5.00%

Ultra-Short-Term Bond

3.95%

Short-Term-Tax-Exempt Bond ETF

2.91%

3.73%

3.83%

4.53%

4.75%

4.92%

Short-Term Treasury ETF

4.30%

Limited-Term Tax-Exempt

3.13%

4.01%

4.12%

4.88%

5.11%

5.29%

Short-Term Treasury

4.11%

Short Duration Tax-Exempt Bond ETF

3.32%

4.26%

4.37%

5.17%

5.42%

5.61%

Short-Term Federal

3.78%

Short-Term Bond ETF

4.47%

Short-Term Corporate ETF

4.86%

Short-Term Inv.-Grade

4.55%

Interm.-Term Tax-Exempt Bond ETF

3.26%

4.18%

4.29%

5.08%

5.33%

5.51%

Intermediate-Term Treasury ETF

4.44%

Interm.-Term Tax-Exempt

3.43%

4.40%

4.51%

5.34%

5.60%

5.79%

Intermediate-Term Treasury

4.27%

Tax-Exempt Bond Index

3.51%

4.50%

4.62%

5.47%

5.74%

5.93%

Intermediate-Term Bond ETF

4.90%

Core Tax-Exempt Bond ETF

3.82%

4.90%

5.03%

5.95%

6.24%

6.45%

Total Bond Market Index

4.57%

Core Bond

4.70%

Intermediate-Term Corporate ETF

5.35%

Intermediate-Term Inv.-Grade

5.16%

Long-Term Tax-Exempt

3.80%

4.87%

5.00%

5.92%

6.21%

6.42%

Long-Term Treasury ETF

4.85%

Long-Term Treasury

4.58%

Long-Term Bond ETF

5.33%

High-Yield Tax-Exempt

4.11%

5.27%

5.41%

6.40%

6.72%

6.94%

Multi-Sector Income

5.66%

Long-Term Corporate ETF

5.79%

Long-Term Invest.-Grade

5.34%

High-Yield Corporate

6.16%

*Tax equivalent yields incorporate the 3.8% health care surtax into the 32%, 35% and 37% tax rates.

Yields as of 1/31/2025. Source: Vanguard and The IVA

Remember that the table above provides a snapshot of yields at the end of January. My rule of thumb is that if you are in one of the top three tax brackets, you should consider owning a municipal bond fund in your brokerage account.

A Formula for Success

Vanguard’s bond fund formula applies to both taxable and municipal bond funds. It is simple, consistent and well-tested: First, keep costs low so the portfolio managers don’t have to take added risk for added income. Then, build plain-vanilla portfolios that deliver competitive yields without, again, taking extra risks.

When it comes to its tax-exempt bond funds, Vanguard manages all assets in-house. I am confident in Vanguard’s ability to execute its core fixed-income strategies well, whether we are discussing its indexed or actively managed funds.

Vanguard’s bond team doesn’t get the credit it deserves. Their success isn’t reliant on a star manager—they benefit much more from structural advantages. That boosts my confidence that they’ll continue to deliver relatively good results year in and year out.

All of the National Tax-Exempt Funds

Vanguard’s “municipal” bond funds generate income that is typically not taxed at the Federal level. Investors in the top three tax brackets may want to consider holding a tax-exempt bond fund as a core bond holding in their taxable (brokerage) accounts.

Vanguard has expanded its lineup over the past few years, launching a handful of index-based and actively managed ETFs (see here). Many of the funds now have similar names. The following two tables are meant to help you keep all the funds (new and old) straight.

The first table below shows each fund’s average maturity, duration and SEC yield. I’ve included the tickers for each fund’s different share classes and whether it is actively managed or index-based.

Comparing National Muni Funds: Risk and Return

Fund

Ticker (Investor / Admiral / ETF)

Active or Index

Maturity

Duration

Yield

Municipal Money Market

VMSXX / – / –

Active

0.04

0.0

2.34%

Ultra-Short-Term Tax-Exempt

VWSTX / VWSUX / –

Active

1.7

1.2

2.96%

Short-Term-Tax-Exempt Bond ETF

– / – / VTES

Index

3.3

2.5

2.91%

Limited-Term Tax-Exempt

VMLTX / VMLUX / –

Active

4.1

2.5

3.13%

Short Duration Tax-Exempt Bond ETF

– / – / VSDM

Active

4.3

2.7

3.32%

Interm.-Term Tax-Exempt Bond ETF

– / – / VTEI

Index

9.1

5.1

3.26%

Interm.-Term Tax-Exempt

VWITX / VWIUX / –

Active

9.8

5.6

3.43%

Tax-Exempt Bond Index

– / – / VTEB

Index

13.9

6.7

3.51%

Core Tax-Exempt Bond ETF

– / – / VCRM

Active

15.1

6.7

3.82%

Long-Term Tax-Exempt

VWLTX / VWLUX / –

Active

17.1

8.0

3.80%

High-Yield Tax-Exempt

VWAHX / VWALX / –

Active

17.1

7.7

4.11%

Yields as of 1/31/2025. Maturity and Duration as of 12/31/2024. Source: Vanguard and The IVA

The table below is a high-level framework I’ve found helpful in keeping Vanguard’s new offerings straight.

Vanguard's Expanded Muni Lineup

Maturity Bucket

Active Mutual Fund

Index Mutual Fund

Active ETF

Index ETF

Ultra-Short

Ultra-Short Tax-Exempt (VWSTX)

—

—

—

Short

Limted-Term Tax-Exempt (VMLTX)

—

Short Duration Tax-Exempt Bond ETF (VSDM)

Short-Term Tax-Exempt Bond ETF

Intermediate

Interm.-Term Tax-Exempt (VWITX)

—

—

Interm.-Term Tax-Exempt Bond ETF (VTEI)

All Maturities

—

Tax-Exempt Bond Index (VTEAX)

Core Tax-Exempt Bond ETF (VCRM)

Tax-Exempt Bond ETF (VTEB)

Long

Long-Term Tax-Exempt (VWLTX)

—

—

—

High-Yield

High-Yield Tax-Exempt Bond (VWAHX)

—

—

—

I’ve started with Vanguard’s “national” tax-exempt funds, which have the broadest appeal. Don’t fear; I’ll discuss Vanguard’s state-specific funds at the end of the article.